San Francisco Bad Faith Insurance Claims Attorney

Table of Contents

Bad Faith Insurance Claims in San Francisco: What You Need to Know

Beyond simple denials, bad faith involves insurers breaching their duty of good faith. If you’re facing a San Francisco Bad Faith Insurance Claims Attorney situation in San Francisco, know that California law protects you. Bad faith means an insurer’s unreasonable denial, delay, or inadequate investigation of a legitimate claim, per California Insurance Code Section 790.03(h). You’re not alone–insurers must act fairly under state regulations.

Common Bad Faith Practices

Insurers in the Bay Area often exhibit these misconducts:

- Failing to promptly communicate claim status on a denied insurance claim.

- Misrepresenting policy benefits to policyholders.

- Offering unreasonably low settlements.

- Denying claims without proper cause, such as in disability insurance denial cases where medical evidence is ignored.

These practices violate fair claims handling standards. San Francisco’s urban density and complex Bay Area policies heighten their prevalence, with local courts applying state law rigorously.

File a complaint with the California Department of Insurance, authoritative state regulatory guidance, via their online form or hotline. Document all communications immediately.

For personalized help, we at McCaslin Law, PC–your San Francisco Bad Faith Insurance Claims Attorneys with 27 years serving Northern California–can navigate litigation. Contact us for next steps.

Understanding Bad Faith Insurance in California

In California, particularly for San Francisco residents, bad faith elevates insurance disputes to legal violations. A San Francisco Bad Faith Insurance Claims Attorney can guide policyholders through these challenges.

What Constitutes Bad Faith Under California Law

Bad faith constitutes a breach of the implied covenant of good faith and fair dealing, as outlined in California Insurance Code §790.03(h). This occurs when insurers prioritize profits over policyholder interests. Key elements include:

- Unreasonable denial of claims without proper investigation.

- Failure to communicate promptly with policyholders.

- Coercive settlement tactics pressuring unfair agreements.

- Misrepresenting policy provisions to avoid payouts.

- Delaying payments beyond reasonable timelines.

- Failing to defend policyholders adequately in litigation.

- Rejecting reasonable settlements within policy limits, per precedents like Comunale v. Traders & General Ins. Co..

The American Bar Association highlights California’s plaintiff-friendly standards in these practices, as authoritative insights from legal professionals on regional variations. Recognizing these elements empowers you to act swiftly.

Signs Your Insurer May Be Acting in Bad Faith

You may notice patterns signaling bad faith during claim handling. These indicators often precede a denied insurance claim. Common signs include:

- Unreasonable delays exceeding 40 days in processing.

- Improper denials lacking substantial evidence or investigation.

- Misrepresenting policy terms to justify rejections.

- Issuing lowball settlement offers far below claim value.

- Ignoring repeated policyholder inquiries.

- Failing to conduct thorough site inspections.

- Coercive tactics like threatening policy cancellation.

For example, delayed property damage payouts after storms exemplify these issues. The California Department of Insurance offers official state guidance on recognizing such behaviors through consumer resources. Document everything to build a strong case.

Icons of common bad faith insurance practices in California

These visuals illustrate frequent violations, helping San Francisco policyholders identify problems early. Awareness prevents escalation and supports timely intervention.

California-Specific Standards for Bad Faith Claims

California Fair Claims Settlement Practices Regulations (10 CCR §2695) mandate prompt investigation and fair dealing. Precedents like Jordan v. Allstate Ins. Co. reinforce insurers’ duties. For San Francisco policyholders facing bad faith, contact an Insurance Bad Faith Attorney San Francisco. Local superior court trends favor thorough documentation. The California Department of Insurance attributes government-mandated procedures for challenging denials via appeal processes. These standards protect Northern California residents effectively.

Bad Faith in Disability and Home Insurance Denials

Disability insurance denial often involves retroactive policy reinterpretation, leading to wrongful benefit terminations. Home insurance rejections for weather damage skip site inspections, ignoring evidence. Patterns include systematic underpayment and evasion. Punitive damages under Cal. Civ. Code §3294 deter such conduct. A San Francisco Bad Faith Insurance Claims Attorney advises on these wrongs. Understanding these patterns is key before pursuing an appeal or lawsuit.

Benefits of Pursuing Bad Faith Insurance Claims

Once bad faith is evident, pursuing claims under California law yields significant benefits for policyholders, such as those facing a denied insurance claim. Consulting a San Francisco Bad Faith Insurance Claims Attorney early empowers strategic action.

Recoverable Damages in Bad Faith Lawsuits

California law allows recovery of multiple damage types in bad faith lawsuits, providing comprehensive remedies for insurer misconduct. Contract damages include unpaid policy benefits plus interest, ensuring policyholders receive full coverage owed. Tort damages cover emotional distress, attorney fees, and litigation costs arising from wrongful handling. Punitive damages target egregious conduct, as outlined in California Insurance Code § 790.03 and precedents like Egan v. Mutual of Omaha, according to American Bar Association expert committee analysis on West Coast practices.

These awards address a disability insurance denial or other bad faith denial of benefits, restoring financial stability. At McCaslin Law, PC, with our 27 years of trial-first mentality, we guide clients through these potentially recoverable remedies.

Strategic Advantages of Litigation

Litigation creates leverage against insurers, compelling fair settlements. Discovery risks pressure carriers to resolve denied insurance claims promptly, avoiding exposure of internal misconduct. California mandates fair claims practices, protecting policyholders from unreasonable delays or denials.

Real-world scenarios illustrate this: In property disputes, insurers settle after facing evidence of bad faith tactics. For a disability insurance denial, negotiation boosts lead to reinstated benefits plus extras. American Bar Association analysis highlights California’s duty to settle within policy limits, enhancing our aggressive advocacy in Northern California courts.

We at McCaslin Law, PC, leverage these protections with meticulous preparation, turning denied insurance claims into favorable outcomes.

Long-Term Benefits for Policyholders

Pursuing bad faith actions improves future claim handling by prompting insurer reforms and training. This deters repeat misconduct, fostering accountability across policies. Policyholders gain heightened awareness of coverage value, strengthening positions in ongoing relationships.

Over time, these efforts enhance industry standards, benefiting all facing a denied insurance claim. Our relentless pursuit at McCaslin Law, PC, with direct attorney involvement, secures lasting protections for Northern California clients.

Case Examples from Northern California

Northern California cases demonstrate tangible benefits. In San Francisco, a property owner overturned a denied insurance claim after fire damage denial, recovering contract benefits, emotional distress awards, and fees through litigation pressure.

Oakland policyholders in a disability insurance denial scenario benefited by hiring an oakland bad faith lawyer, securing multi-million settlements without trial, as seen in similar precedents. These examples, drawn from regional practices per American Bar Association insights, show potential without guaranteeing results.

These benefits underscore why consulting local experts like a San Francisco Bad Faith Insurance Claims Attorney matters, leading into qualification steps.

How Bad Faith Insurance Claims Work in San Francisco

After confirming bad faith in your denied insurance claim in San Francisco, consulting a San Francisco Bad Faith Insurance Claims Attorney becomes essential for navigating the complex process. We at McCaslin Law, PC, with our trial-first mentality, outline the key steps ahead to empower policyholders facing insurer misconduct.

Steps After a Suspected Bad Faith Denial

Document all communications meticulously. Begin by gathering every email, letter, phone log, and policy document related to your claim. Review your policy terms closely to identify any unreasonable denial basis.

Send a formal dispute letter. Outline the bad faith indicators, demand reconsideration, and set a 30-day response deadline. According to the California Department of Insurance, thorough records strengthen your position.

Check for insurer delays. Note any undue procrastination in processing, a common bad faith tactic in denied insurance claims.

Notify the California Department of Insurance if needed. File a complaint for oversight, as state regulatory guidelines for consumer appeals recommend.

These initial actions lay a strong foundation, preventing evidence loss and signaling resolve to the insurer.

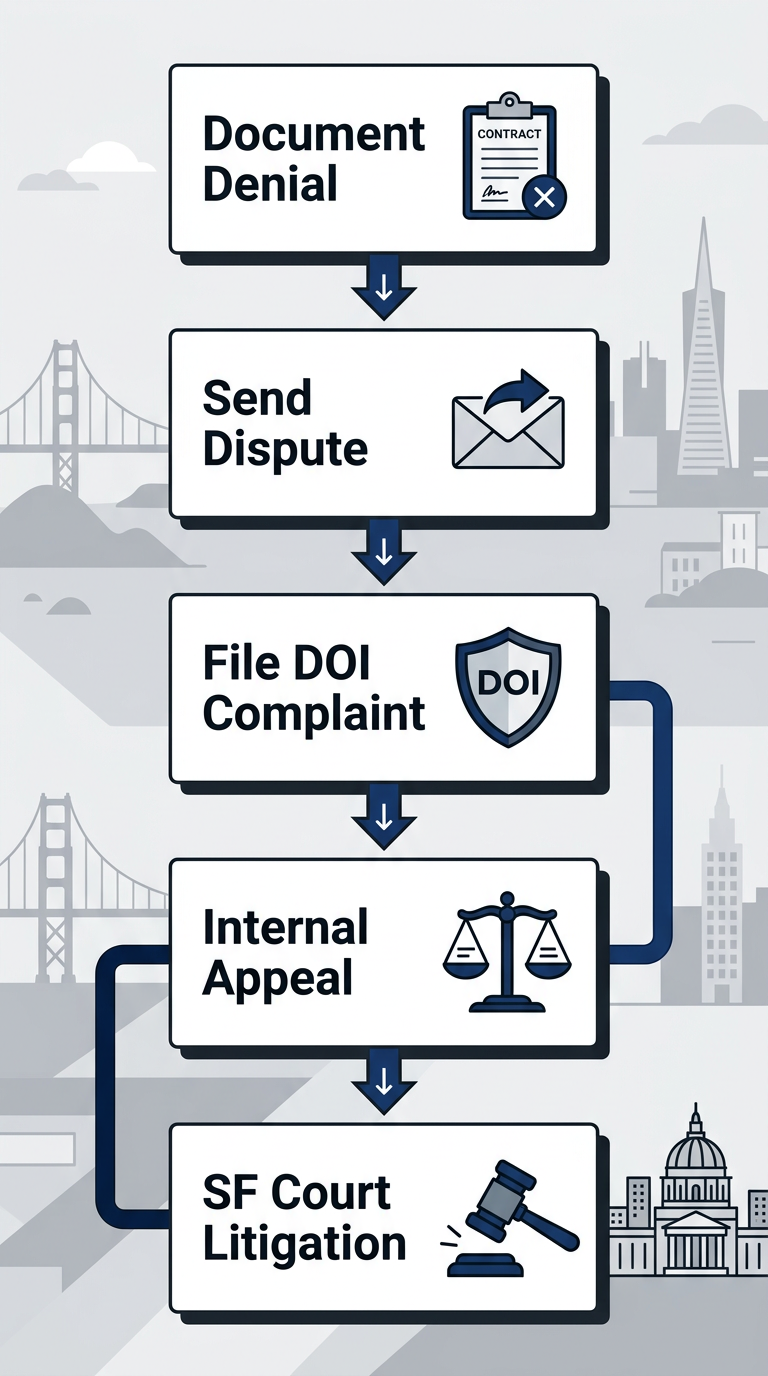

5-stage process for bad faith insurance claims appeals in San Francisco

This visual roadmap illustrates the progression from denial to resolution, helping claimants visualize their path forward in San Francisco courts.

Statute of Limitations for Filing in San Francisco

California imposes strict timelines on bad faith claims. Breach of contract claims carry a 2-year statute of limitations under Code of Civil Procedure § 337, starting from denial accrual. Bad faith tort claims allow 4 years per § 343.

File in San Francisco Superior Court, serving the insurer promptly. Tolling exceptions apply during internal appeals or DOI complaints, extending deadlines as per California Department of Insurance guidelines.

- Day 0: Claim denial received.

- Months 1-24: Contract breach window.

- Up to 48 months: Tort bad faith filing.

- Post-appeal: Tolled periods added.

“Timely action preserves your rights,” notes the official consumer guide from California Department of Insurance on claim processes.

Adhering to these prevents barred claims, ensuring access to justice.

The Litigation Process from Demand to Trial

Bad faith litigation in San Francisco demands a structured approach with our aggressive, trial-focused representation.

- Pre-suit demand package: Compile evidence of denial misconduct and policy violations; send to insurer.

- File complaint: Lodge in San Francisco Superior Court, alleging breach and tortious bad faith.

- Discovery phase: Exchange documents, depositions; motions challenge insurer defenses–here, contact an insurance claims attorney sacramento for complex support.

- Settlement conference: Mandatory mediation tests resolution viability.

- Jury trial: Emphasize trial-first preparation, presenting punitive damages evidence.

This sequence, guided by meticulous preparation, pressures insurers toward fair settlements while readying for courtroom victory.

Appealing Denied Claims Before Suing

Exhaust pre-litigation options to bolster your case. Insurer internal appeals must be filed within 60 days of denial, per fair claims practices.

California Department of Insurance complaint: Submit detailed records online or mail; authoritative state regulatory guidelines outline procedures, requiring response within set timelines.

- Step 1: Request internal review with all evidence.

- Step 2: If denied, file DOI complaint citing violations.

- Step 3: Report Fair Claims Settlement Practices infractions.

For disability insurance denial scenarios, these steps apply similarly.

“Consumers should first complain to the insurer,” advises California Department of Insurance on appeals.

If unresolved, engage a San Francisco Bad Faith Insurance Claims Attorney next for litigation readiness.

Best Practices for Handling Denied Insurance Claims

Documenting Your Claim Thoroughly

Building on common denial triggers, documenting your denied insurance claim thoroughly lays the foundation for successful resolution, whether appealing independently or consulting a San Francisco Bad Faith Insurance Claims Attorney in San Francisco. As California Department of Insurance official state consumer protection guidelines emphasize, meticulous records empower policyholders against insurers.

- Retain the original denial letter with the date received.

- Compile dated medical records and bills.

- Log all insurer communications with timestamps and reference numbers.

- Photograph physical evidence like property damage.

- Obtain witness affidavits if applicable.

- Create a timeline spreadsheet of claim events.

This comprehensive approach ensures you have irrefutable evidence ready for the next steps. Once documented, proceed to appeals promptly to protect your legal options and preserve evidence.

Effective Appeal Strategies

Crafting a strong appeal transforms a denied insurance claim into an opportunity for approval. California Department of Insurance authoritative procedures for health claim appeals outline clear paths to success.

Follow this 4-step process:

- Review denial reasons within 180 days.

- Gather additional supporting documents like independent medical opinions.

- Write a concise appeal letter citing policy language and California Insurance Code Section 10123.3.

- Submit via certified mail with tracking.

Persistence pays off; track submissions closely to avoid delays. These steps address the insurance claim denial process effectively.

When to Consult a Bad Faith Attorney

Escalation becomes essential when insurers exhibit bad faith patterns in handling your denied insurance claim. Watch for these 5 red flags signaling potential violations under California law:

- Repeated denials without explanation.

- Undue delays beyond 30 days.

- Lowball settlement offers ignoring policy limits.

- Failure to investigate claim promptly.

- Pressure to accept release forms.

For disability insurance denial intertwined with bad faith, or complex cases, seek a San Francisco Bad Faith Insurance Claims Attorney in San Francisco immediately. We recommend consulting a personal injury attorney san francisco for expert legal help in personal injury-related bad faith claims.

Special Considerations for Disability Denials

Disability insurance denial requires tailored strategies due to federal and state overlays. ERISA preempts federal employer plans, while California protections apply to individual policies; California Employment Development Department state agency protocols for disability appeals dictate strict timelines.

Key actions include:

- Appeal EDD SDI denials within 30 days using Form DE 1000A.

- Include functional capacity evaluations.

- Add vocational expert reports.

- Submit via myEDD for faster processing.

Late appeals may qualify with good cause, strengthening your denied disability benefits case significantly.

Taking Action on Your San Francisco Insurance Dispute

Once you’ve confirmed a potential bad faith issue with a denied insurance claim in San Francisco, act swiftly to protect your rights. A San Francisco Bad Faith Insurance Claims Attorney can guide complex cases, but start with these essential steps outlined by the California Department of Insurance.

Follow this structured process:

- Gather documentation: Collect your policy, denial letters, and all correspondence immediately.

- Pursue internal appeal: Contact your insurer within their specified timeline, typically 30-60 days for responses, as per California Department of Insurance procedures.

- File a complaint online: Submit to the California Department of Insurance with policy number, insurer details, and dispute description–authoritative state regulatory guidance ensures consumer protection.

- Document everything: Track all communications for potential escalation, especially in a disability insurance denial scenario.

When bad faith persists, consult professionals. At McCaslin Law, PC, with over 25 years of trial-focused representation, we offer free consultations for complex disputes, including real estate insurance issues. Reach out to a san francisco real estate litigation lawyer today. We offer a free confidential consultation to evaluate your insurance dispute right away.

This article was researched and written with the assistance of AI tools.