San Francisco Insurance Bad Faith Attorney

Table of Contents

Insurance Bad Faith Claims in San Francisco, California

In San Francisco, California, insurance bad faith arises when insurers unreasonably deny, delay, or fail to investigate claims, violating California Insurance Code Section 790 et seq. A San Francisco Insurance Bad Faith Attorney helps policyholders enforce their rights under strict state regulations. These issues affect many in the San Francisco Bay Area facing unfair treatment.

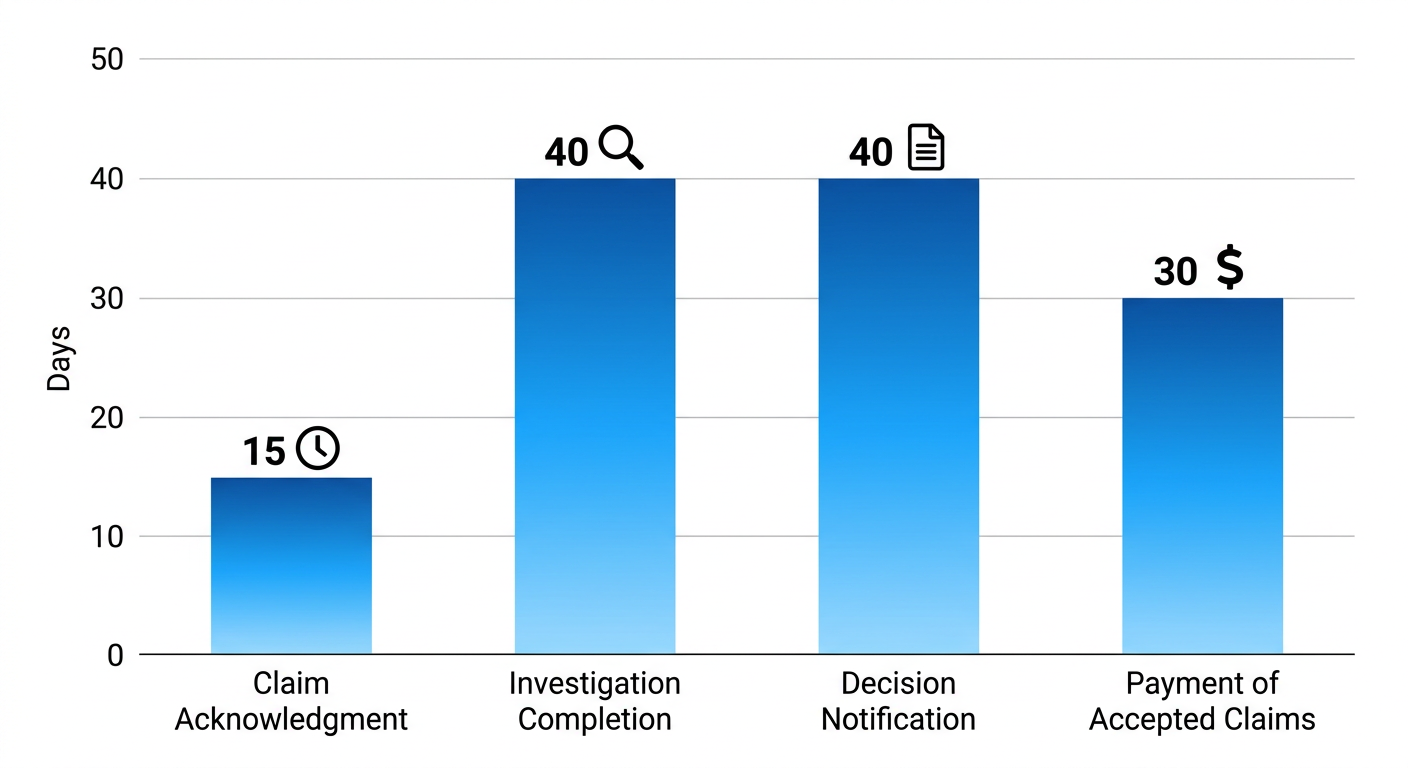

The California Department of Insurance mandates fair claims settlement timelines: insurers must acknowledge claims within 15 days, complete investigations within 40 days, notify decisions within 40 days, and pay accepted claims within 30 days. Violations like bad faith claim denial in property or auto insurance, or delayed insurance claim payment in health disputes, trigger liability. San Francisco Superior Court handles these cases, protecting local policyholders from unreasonable delays.

California fair claims settlement timelines for insurance bad faith prevention

Policyholders can seek compensatory damages, punitive awards, and attorney fees. With over 27 years serving Northern California, we at McCaslin Law, PC, provide trial-focused representation. Contact a reputable Sacramento litigation firm like ours for bad faith claims in San Francisco, California. Learn more about filing processes next.

Defining Insurance Bad Faith Under California Law

Under California law specifically, insurers must uphold duties of good faith and fair dealing, as established in landmark cases like Royal Globe and Moradi-Shalal. We at McCaslin Law, PC, with 27 years serving Northern California, help policyholders in San Francisco navigate these obligations. A San Francisco Insurance Bad Faith Attorney can assess your situation early.

What Qualifies as Insurance Bad Faith in California

California Insurance Code §790.03 and §790.05, enforced as binding state regulatory standards by the California Department of Insurance, outline unfair practices constituting bad faith. These include failure to establish standards for prompt investigation of claims within 40 days, as per Title 10 CCR §2695.5. Insurers also violate by not communicating acceptance or denial within 40 days, misrepresenting pertinent policy provisions, and failing to provide prompt, reasonable explanations for denials.

Other violations encompass not attempting good faith settlements when liability is clear and not paying undisputed benefits within 30 days. The California Department of Insurance’s Fair Claims Settlement Regulations detail these timelines, protecting consumers from unjustified bad faith claim denial. If you’re facing this, recognize these legal benchmarks to build a strong case.

Beyond definitions, watch for these signs in your interactions with your insurer.

Signs Your Insurer May Be Acting in Bad Faith

Common indicators of insurer misconduct include:

- Unreasonable delays exceeding 40 days in investigation or response, leading to unreasonable delayed insurance claim payment.

- Denial without adequate investigation or reasonable basis, amounting to insurer bad faith denial.

- Lowball settlement offers that undervalue your claim.

- Failure to pay undisputed benefits within 30 days, per California Department of Insurance consumer protection resources.

- Ignoring applicable policy limits or coverages.

- Pressuring claimants to accept less than deserved.

- Poor communication, such as evading policyholder inquiries.

These align with official guidance from the California Department of Insurance on recognizing violations like communication failures. Contact a San Francisco Insurance Bad Faith Attorney if you spot these signs. For instance, mishandling specialized claims, akin to delays in in-home ABA therapy Utah, exemplifies how insurers may drag out payments unreasonably, mirroring California bad faith delay tactics.

Timing is critical: know your deadlines to preserve rights.

Statute of Limitations for Bad Faith Claims

California imposes a 2-year statute of limitations for bad faith claims under Code of Civil Procedure §339(1), starting from discovery of the injury-causing conduct. Accrual typically begins upon receipt of a denial letter triggering a bad faith claim denial, or when facts reveal unreasonable delay. For example, if an insurer’s unjustified denial arrives in January 2024, you must file by January 2026.

Tolling exceptions apply only for fraud concealment, not standard delays. California Department of Insurance resources emphasize prompt action to avoid barred claims. We advise documenting all interactions meticulously. Once confirmed, act within limits–consult a San Francisco Insurance Bad Faith Attorney immediately for evaluation.

Potential Damages in Bad Faith Lawsuits

With bad faith proven, focus shifts to potential damages, which determine the true value of a lawsuit. These awards compensate policyholders for insurer misconduct and deter future violations. Consulting a San Francisco Insurance Bad Faith Attorney early maximizes recovery in California cases, where courts scrutinize unreasonable denials and delays.

Types of Recoverable Damages

Bad faith lawsuits allow recovery of multiple damage types beyond standard policy benefits. We guide clients through these to secure full compensation.

- Compensatory damages cover direct economic losses, such as unpaid medical bills after an accident or property repair costs from storm damage.

- Consequential damages address indirect harms, like lost wages from delayed payments or damaged credit scores affecting loans.

- Emotional distress damages compensate non-economic injury, such as severe anxiety proven by therapy records or depression linked to financial ruin.

- Punitive damages punish reckless behavior, awarded when insurers ignore clear liability.

Document all losses meticulously. This strengthens claims and supports higher awards.

Damages Specific to Claim Denials

Bad faith claim denials trigger recovery of full policy benefits plus extras. Courts award these when insurers breach their duty to pay valid claims promptly.

Consider a homeowner denied flood coverage despite clear policy terms; they recover the home value, attorney fees, and pre-judgment interest on overdue sums. In another scenario, a business faces bad faith claim denial for equipment breakdown, gaining policy limits plus costs for temporary rentals and lost revenue. The American Bar Association provides authoritative professional guidance on insurer duties, noting breaches like failing to settle within policy limits lead to excess judgments and extra-contractual damages.

A third case involves medical claims ignored, yielding benefits plus hardship expenses. Always demand written explanations from carriers. This preserves evidence for litigation.

Punitive Damages for Delays and Bad Faith

Punitive damages apply to egregious conduct, such as delayed insurance claim payment exceeding 30-60 days without cause or ignoring undisputed amounts. California requires clear and convincing evidence of malice, like rejecting settlements within policy limits despite strong liability evidence.

For instance, an auto insurer delays payout post-crash, forcing our client into excess judgment; punitive awards followed per American Bar Association insights on duty to settle. Another trigger: unreasonable investigation delays breaching good faith covenants, capped in some states but potent for deterrence.

Triggers include setup-like demands ignored or poor documentation. Gather timelines and communications. Expert testimony bolsters malice proof for maximum punitive recovery.

Understanding these damages underscores why partnering with experienced counsel like McCaslin Law, PC is crucial. With our trial-first mentality and 27 years serving Northern California, we maximize awards. Firms offering bad faith representation often handle related areas like defective products–see a San Francisco Defective Products Lawyer for comprehensive litigation support, leading into filing strategies next.

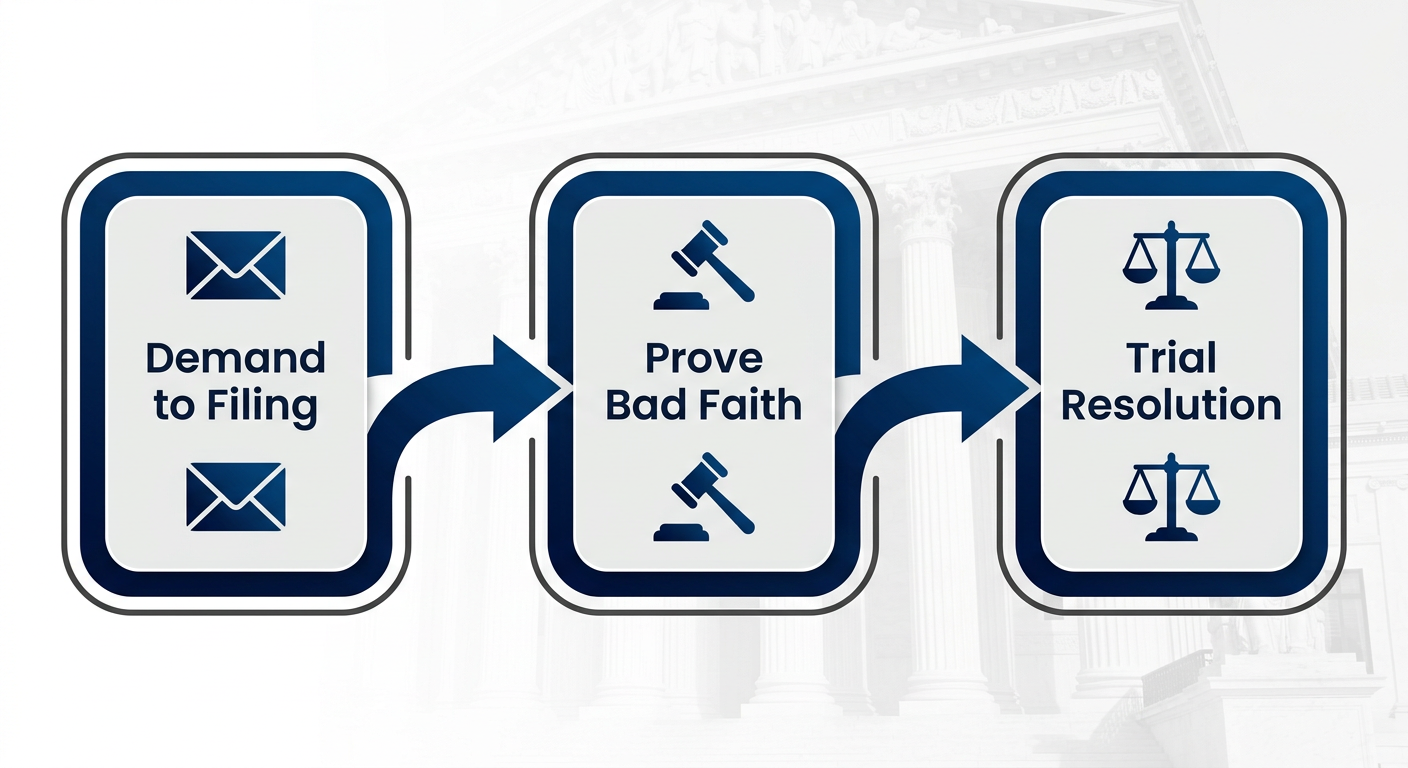

The Insurance Bad Faith Litigation Process

Once bad faith is clear, the litigation process begins with strategic pre-litigation steps. At McCaslin Law, PC, with our trial-first mentality, we guide clients through this as premier San Francisco Insurance Bad Faith Attorneys serving Northern California. Our 27 years of experience ensure aggressive advocacy against bad faith claim denial and delayed insurance claim payment.

Insurance bad faith litigation process stages visualization

This visual outlines the key stages we navigate, from demand to resolution, empowering you to understand each phase.

From Demand Letter to Filing Suit

Sending a detailed demand letter is the first formal step. Outline the insurer’s breaches, such as unreasonable denial or delay in processing claims. Demand fair compensation and a response timeline.

- Pre-litigation negotiation: Engage directly with adjusters to resolve delayed insurance claim payments amicably.

- Mediation options: Utilize the California Department of Insurance Auto Mediation Program, a free, voluntary process for disputes over $7,500 where insurers cover costs, according to the California Department of Insurance.

- Attorney involvement: Contact us early, especially after initial bad faith claim denial or stalled negotiations, to avoid time-barred claims.

These steps often prompt settlements, but persistent insurers require suit. We prepare meticulously for this transition.

Proving Bad Faith in Court

Gathering compelling evidence is crucial to establish insurer misconduct.

- Internal documents: Secure emails, claims notes revealing improper motives in bad faith claim denial.

- Expert testimony: Industry specialists affirm breaches of standards like timely payments.

- Overcome summary judgment: Demonstrate triable issues, as in the Santa Barbara Superior Court tentative ruling in case 23CV00285-6, denying motions by showing factual disputes despite policy limits challenges.

For instance, in complex claims like Golden Touch ABA therapy, we expose insurer tactics in therapy denials, illustrating bad faith patterns. Our meticulous preparation ensures survival of dismissal motions.

Trial Preparation and Resolution

We employ our trial-first strategy, pushing for jury trials in Northern California courts like those in San Francisco. As your San Francisco Insurance Bad Faith Attorney, we lead discovery and motions practice relentlessly.

Preparation includes depositions, exhibit organization, and mock trials. Settlement negotiations intensify pre-trial, leveraging our aggressive posture. Resolutions come via favorable verdicts, strategic settlements, or appeal avoidance through strong positioning.

Our direct attorney involvement delivers excellence in litigation. We pursue maximum available compensation through focused litigation, thorough proof development, and vigorous courtroom advocacy on your behalf. Successful resolution often yields substantial recoveries, positioning clients for recovery as detailed in the next section.

Protecting Your Rights Against Bad Faith Practices

Once you identify signs of bad faith, protect yourself by documenting everything and responding decisively. At McCaslin Law, PC, with our 27 years of experience handling insurance claims litigation across Northern California, including San Francisco, we guide policyholders through these challenges. Consulting a San Francisco Insurance Bad Faith Attorney early strengthens your position.

Documenting Denials and Delays

Meticulous record-keeping forms the foundation of a strong case against bad faith claim denial or delayed insurance claim payment, as recommended by the California Department of Insurance’s consumer protection advice.

- Keep dated copies of all claim submissions, including forms, photos of damages, and medical records if applicable.

- Save every piece of insurer correspondence, such as emails, letters, and denial notices with specific reasons.

- Log phone calls with dates, times, adjuster names, and detailed summaries of discussions.

- Create a timeline of interactions to highlight patterns of unreasonable delays.

- Photograph ongoing damages periodically to show progression.

California Department of Insurance regulations require insurers to acknowledge claims within 15 days. Compile these records now to build irrefutable evidence. If delays persist, contact us to review your documentation for potential bad faith action.

Responding to Insurer Tactics

When facing unreasonable denials or delays, take swift, structured steps to enforce your rights under state law, potentially with support from a San Francisco Insurance Bad Faith Attorney.

- Send a certified demand letter citing specific violations of California Insurance Code fair claims settlement regulations, like the 40-day decision deadline.

- File a formal complaint with the California Department of Insurance via their online portal or hotline at 1-800-927-4357, referencing official consumer guidance.

- Consult a bad faith attorney within statutory limits to evaluate appraisal or litigation options.

- Demand payment of undisputed amounts promptly, as mandated by binding state regulations.

- Reject lowball offers without written justification.

These actions pressure insurers to comply. We at McCaslin Law, PC, apply our trial-first mentality to such responses, ensuring aggressive advocacy. Escalate immediately if tactics continue.

Examples of Bad Faith by Insurers

Insurers employ common tactics violating fair claims settlement regulations, such as failing to acknowledge claims within 15 days or misrepresenting policy terms, which you can counter effectively.

- Lowball offers: Proposing inadequate settlements without evidence; respond by demanding detailed justification and invoking regulations for prompt payment of undisputed portions.

- Unnecessary post-deadline investigations: Dragging out probes beyond 40 days; document the delays and file a CDI complaint per consumer protection advice.

- Failure to acknowledge or decide timely: Ignoring claims or delaying decisions; cite California Department of Insurance timelines in a demand letter.

- Denials of specialized therapies, similar to denials of ABA therapy children Utah, often lack proper reasoning; gather medical evidence and threaten bad faith litigation.

Track these patterns rigorously. If tactics persist, escalate to formal claims with our team’s meticulous preparation.

Next Steps for Bad Faith Insurance Disputes

Once bad faith is evident from claim denials or delays, such as bad faith claim denial or delayed insurance claim payment, policyholders must act swiftly. Consulting a San Francisco Insurance Bad Faith Attorney early can uncover violations of the insurer’s duty to settle within policy limits, as outlined by the American Bar Association.

Follow these critical steps:

- Document all evidence immediately, including correspondence, claim denial letters, and records of delayed insurance claim payments.

- Send a formal written demand to the insurer detailing the bad faith conduct, like failure to settle reasonable policy limits demands.

- Schedule a consultation with a bad faith insurance lawyer in San Francisco to assess case strength and punitive damages potential.

- Prepare for litigation: Gather evidence, file in state court, and invoke the insurer’s duty to settle per American Bar Association guidance on time limit demands.

- Act before statutes of limitations expire–typically 2-4 years by state–by hiring experienced counsel to negotiate or litigate effectively.

At McCaslin Law, PC, with our 27 years of trial-focused representation, we guide clients through these disputes. Take the first step today by reaching out to a San Francisco Real Estate Litigation Lawyer for specialized consultation on bad faith claims.

This article was researched and written with the assistance of AI tools.

Resources

Review Tentative Ruling Denying Summary Judgment in Bad Faith Case

Explore California Fair Claims Settlement Practices Regulations

Learn California’s Automobile Claims Mediation Program Details

Get Help Filing Insurance Complaints with California DOI